Roth IRA Conversions 2026: Ultimate Guide & Analysis

Anúncios

This article provides an in-depth look into Roth IRA Conversions 2026, offering essential insights for your retirement strategy. We explore the benefits, potential drawbacks, and key considerations to help you navigate this complex financial decision. Our analysis focuses on current trends and expert recommendations to ensure you have the most relevant information at hand.

The financial landscape is ever-evolving, and understanding the nuances of retirement planning is more critical than ever. For many, a Roth IRA Conversion 2026 could be a pivotal strategy in optimizing their long-term savings.

This comprehensive guide delves into the specifics of converting a traditional IRA to a Roth IRA, examining the potential tax implications, eligibility requirements, and strategic timing for such a move. We aim to equip you with the knowledge needed to assess if this financial maneuver aligns with your individual retirement goals.

Anúncios

Understanding Roth IRA Conversions: The Basics for 2026

A Roth IRA conversion involves moving funds from a traditional, SEP, or SIMPLE IRA into a Roth IRA. This action is typically motivated by the desire to enjoy tax-free withdrawals in retirement, a significant advantage over the taxable distributions of traditional IRAs.

While the concept remains consistent, the economic and legislative environment of 2026 could introduce specific considerations that impact the optimal timing and overall benefit of a conversion. It’s crucial to evaluate these factors carefully before proceeding.

The decision to convert is not one-size-fits-all; it depends heavily on your current income, future tax expectations, and overall financial strategy. Understanding the fundamental mechanics is the first step toward making an informed choice.

Anúncios

What is a Roth IRA and How Does it Differ?

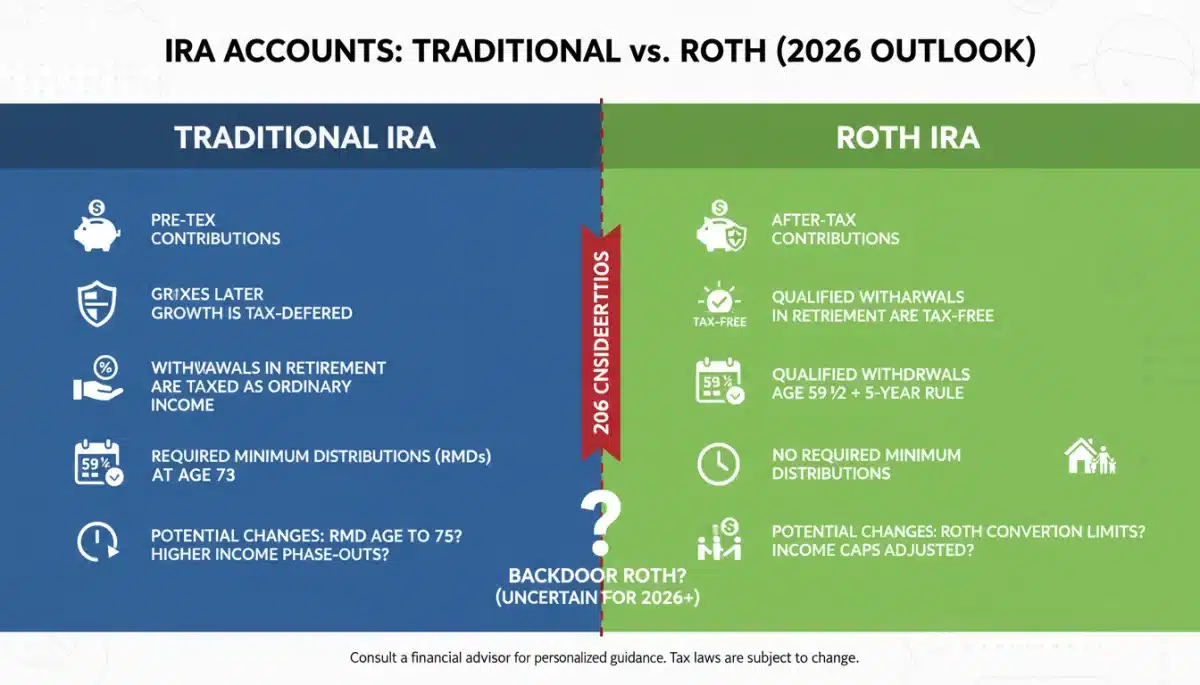

A Roth IRA is an individual retirement account that allows qualified withdrawals to be tax-free in retirement. Contributions to a Roth IRA are made with after-tax dollars, meaning you pay taxes on the money now, not when you take it out later.

This contrasts sharply with a traditional IRA, where contributions may be tax-deductible, and withdrawals in retirement are typically taxed as ordinary income. The key distinction lies in when you pay taxes on your retirement savings.

The appeal of a Roth IRA lies in its ability to shield your investment growth and withdrawals from future tax liabilities, which can be particularly advantageous if you anticipate being in a higher tax bracket during retirement.

- Tax Treatment: After-tax contributions, tax-free withdrawals in retirement.

- Contribution Limits: Subject to annual IRS limits (which may be adjusted for 2026).

- Withdrawal Rules: Qualified distributions are tax-free after age 59½ and the account has been open for at least five years.

The Mechanics of a Roth Conversion

Converting a traditional IRA to a Roth IRA involves transferring the assets from one account type to another. This process triggers a taxable event for any pre-tax contributions and earnings within the traditional IRA.

The amount converted is added to your taxable income for the year of conversion, potentially pushing you into a higher tax bracket. Therefore, careful tax planning is essential to mitigate immediate financial impact.

While the tax hit can be significant in the conversion year, the long-term benefits of tax-free growth and withdrawals in retirement often outweigh this initial cost, especially for those with a long investment horizon.

Key Considerations for Roth IRA Conversions in 2026

Several factors should influence your decision regarding a Roth IRA Conversion 2026. These include your current income, anticipated future tax rates, and the timeline until your retirement.

The economic outlook for 2026, including potential changes in tax legislation, could significantly alter the attractiveness of a conversion. Staying informed about these developments is paramount for strategic planning.

Additionally, your personal financial situation, including other sources of retirement income and your overall asset allocation, plays a critical role in determining the suitability of a Roth conversion.

Current and Future Tax Brackets

One of the most crucial elements in evaluating a Roth conversion is comparing your current tax bracket to your anticipated tax bracket in retirement. If you expect to be in a higher tax bracket later, converting now could save you money in the long run.

Conversely, if you expect your income to decrease significantly in retirement, and thus your tax bracket to be lower, a traditional IRA might be more advantageous. This projection requires careful foresight and potentially professional guidance.

Tax legislation changes are always a possibility, and any shifts in tax rates or brackets for 2026 could impact the calculus of a Roth conversion. It’s wise to consider various scenarios.

- Lower Current Tax Bracket: Ideal time to convert, paying taxes at a reduced rate.

- Higher Future Tax Bracket: Maximizes tax-free growth and withdrawals later.

- Legislative Changes: Monitor potential tax law reforms for 2026 and beyond.

The Five-Year Rule and Access to Funds

A critical aspect of Roth IRAs is the five-year rule, which dictates that your Roth IRA must be open for at least five years before qualified distributions can be made tax-free. This rule applies to both contributions and conversions.

For conversions, a separate five-year period begins from January 1st of the year you complete the conversion. This means that even if your original Roth IRA was opened more than five years ago, the converted amount has its own five-year clock.

Understanding this rule is vital for liquidity planning. While you can withdraw converted principal tax-free and penalty-free at any time, withdrawing earnings before meeting the five-year rule or age 59½ can incur taxes and penalties.

Analyzing the Pros and Cons of a Roth Conversion

A Roth IRA Conversion 2026 offers several compelling benefits, primarily centered around tax advantages. However, it also comes with potential drawbacks that must be carefully weighed against these benefits.

The decision requires a thorough comparison of the immediate costs versus the long-term gains. It’s not just about taxes, but also about flexibility, estate planning, and your overall financial peace of mind.

An objective analysis of both sides will provide a clearer picture of whether a Roth conversion is the right strategic move for your retirement savings.

Advantages of a Roth Conversion

The primary advantage of a Roth conversion is the ability to enjoy tax-free withdrawals in retirement. This means that all future growth on the converted amount will be completely free from federal income taxes, and often state taxes too.

Another significant benefit is the avoidance of Required Minimum Distributions (RMDs) for the original owner of a Roth IRA. This provides greater control over your retirement funds and allows for continued tax-free growth throughout your lifetime.

Roth IRAs also offer excellent estate planning advantages. Beneficiaries can inherit the Roth IRA and take tax-free withdrawals, making it a powerful tool for intergenerational wealth transfer.

Potential Disadvantages and Risks

The most immediate disadvantage is the tax bill incurred during the year of conversion. This can be substantial if you convert a large sum, potentially pushing you into a higher tax bracket for that year.

Another risk is the uncertainty of future tax rates. If tax rates decrease significantly in the future, you might have paid more taxes upfront than necessary. However, historical trends suggest tax rates are more likely to rise.

Finally, if you need access to the converted funds within five years of the conversion, you could face penalties and taxes on the earnings. This loss of immediate liquidity is an important consideration.

Strategic Timing for a Roth IRA Conversion in 2026

Timing is a critical component of a successful Roth IRA Conversion 2026. The optimal moment to convert often aligns with specific financial or economic conditions that can minimize the tax impact.

Consider periods when your income is lower, perhaps due to a career change, sabbatical, or early retirement. This can allow you to convert funds at a lower marginal tax rate, making the conversion more cost-effective.

Market downturns can also present a strategic opportunity. When your IRA assets have decreased in value, converting them means you’ll pay taxes on a smaller amount, and the subsequent recovery will be tax-free.

When Your Income is Lower

Converting during a year when your taxable income is unusually low can be highly beneficial. This scenario might occur if you take a leave of absence, experience a temporary reduction in work hours, or are between jobs.

By converting when you’re in a lower tax bracket, you minimize the immediate tax liability associated with the conversion. This strategy can significantly enhance the long-term value of your Roth IRA.

Planning for such a conversion requires foresight and careful income management throughout the year to ensure you stay within your desired tax bracket.

During Market Downturns

A counterintuitive but powerful strategy is to convert during a market downturn. When your traditional IRA assets have declined in value, the amount you convert and pay taxes on will be lower.

As the market recovers, the growth on those converted assets within your Roth IRA will be entirely tax-free. This allows you to capitalize on future market appreciation without incurring additional tax liabilities.

This strategy requires a degree of risk tolerance and the ability to act decisively during volatile market conditions. However, the potential rewards can be substantial for your Roth IRA Conversion 2026.

Navigating the Tax Implications of Conversion

The tax implications are arguably the most complex aspect of a Roth IRA Conversion 2026. Understanding how the IRS treats converted funds is essential to avoid unexpected tax bills.

All pre-tax contributions and earnings converted from a traditional IRA to a Roth IRA are subject to federal income tax in the year of conversion. This can significantly increase your taxable income.

It’s crucial to plan for this tax liability, either by paying it from non-retirement funds or by setting aside enough money to cover the taxes. Using converted funds to pay the tax bill is generally not recommended as it reduces your retirement savings and can incur penalties if you are under 59½.

Calculating Your Taxable Income from Conversion

The amount of your conversion that is taxable depends on whether your traditional IRA contains any after-tax contributions. If all contributions were pre-tax (deductible), then the entire converted amount is taxable.

If you have made non-deductible contributions to your traditional IRA, a portion of your conversion will be tax-free. The IRS uses a pro-rata rule to determine the taxable and non-taxable portions of your conversion, which can be complex.

Working with a tax professional or financial advisor is highly recommended to accurately calculate your taxable income from a Roth conversion and to understand any potential state tax implications.

Avoiding Common Conversion Mistakes

One common mistake is failing to account for the tax bill. Many individuals convert funds without having sufficient non-retirement assets to pay the resulting taxes, leading to forced withdrawals from the converted amount.

Another error is converting too much in a single year, which can push you into a significantly higher tax bracket. A phased conversion strategy, converting smaller amounts over several years, can often be more tax-efficient.

Lastly, miscalculating the five-year rule for withdrawals can lead to unexpected penalties. Always ensure you understand the specific timelines for accessing converted funds without penalty.

Comparison: Roth IRA vs. Traditional IRA in 2026 Planning

When considering your retirement savings strategy for 2026, a direct comparison between Roth IRAs and Traditional IRAs is indispensable. Each offers distinct advantages based on your financial situation and future expectations.

The choice between contributing to a traditional IRA versus a Roth IRA, or performing a conversion, hinges on your outlook on future tax rates and your current income level. It’s a strategic decision with long-term implications.

This comparison helps clarify which vehicle might be more beneficial for your specific goals, particularly as tax laws and economic conditions may evolve by 2026.

When a Roth IRA Might Be Better

A Roth IRA is generally more advantageous if you expect to be in a higher tax bracket in retirement than you are now. By paying taxes on your contributions today, you lock in current rates and enjoy tax-free withdrawals later.

If you anticipate significant growth in your investments, the tax-free growth and withdrawals of a Roth IRA can lead to substantial savings over time. This is particularly powerful for younger investors with a long time horizon.

Furthermore, the absence of Required Minimum Distributions (RMDs) for the original owner makes Roth IRAs an attractive option for those who want maximum flexibility in managing their retirement income and leaving a legacy.

When a Traditional IRA Might Be Preferred

A traditional IRA might be more suitable if you expect to be in a lower tax bracket during retirement. The upfront tax deduction on contributions can provide immediate tax savings, which can be significant if you are currently in a high tax bracket.

If you need to lower your current taxable income, deductible traditional IRA contributions can help achieve that goal. This can be a valuable strategy for managing your annual tax liability.

For those who are unsure about their future tax situation or prefer to defer taxes for as long as possible, a traditional IRA offers that flexibility, with taxes paid only upon withdrawal in retirement.

Who Should Consider a Roth IRA Conversion in 2026?

Determining if a Roth IRA Conversion 2026 is right for you involves assessing your unique financial circumstances and future projections. It’s not a universal solution but a strategic move for specific profiles.

Individuals who anticipate higher earnings or higher tax rates in retirement are prime candidates for a Roth conversion. Those with a long time horizon until retirement also stand to benefit significantly from tax-free growth.

Ultimately, the decision should be part of a broader, well-thought-out financial plan, often developed in consultation with a qualified financial advisor.

High-Income Earners Expecting Continued Growth

If you are a high-income earner who is currently above the income limits for direct Roth IRA contributions, the “backdoor Roth” strategy, which involves converting a non-deductible traditional IRA contribution to a Roth, can be very appealing.

For those who expect their income to continue growing or believe tax rates will increase in the future, converting now allows them to pay taxes at potentially lower current rates. This locks in the tax-free status of their retirement funds.

This group often includes younger professionals or individuals in the peak of their careers who have considerable time for their Roth IRA assets to grow tax-free.

Those Planning for Estate or Legacy Planning

Roth IRAs are exceptional tools for estate planning. Since Roth IRAs do not have RMDs for the original owner, the funds can continue to grow tax-free throughout the owner’s lifetime.

Upon the owner’s death, beneficiaries can inherit the Roth IRA and generally take tax-free withdrawals, subject to certain rules. This makes Roth IRAs a powerful vehicle for transferring wealth to future generations without additional tax burdens.

For individuals focused on leaving a substantial, tax-efficient legacy, a Roth IRA Conversion 2026 can be a cornerstone of their estate plan.

Expert Insights and Recommendations for 2026

Financial experts consistently emphasize the importance of personalized advice when considering a Roth IRA Conversion 2026. Generic strategies rarely fit everyone’s unique financial picture.

The consensus among advisors is to conduct a thorough analysis of your current and projected financial situation, including income, tax brackets, and investment goals. This forms the foundation for any sound conversion decision.

Staying abreast of potential legislative changes affecting retirement accounts and tax laws for 2026 is also a key recommendation. These changes could significantly alter the benefits and drawbacks of a conversion.

Consulting a Financial Advisor

Engaging with a qualified financial advisor is paramount before undertaking a Roth IRA conversion. An advisor can help you analyze your specific situation, project future tax liabilities, and develop a tailored strategy.

They can also assist with the complex calculations involved in determining the taxable portion of your conversion and help you understand the long-term impact on your overall retirement plan.

A good advisor will consider all aspects of your financial life, including other retirement accounts, investment portfolio, and estate planning objectives, to ensure a Roth conversion aligns with your broader goals.

Staying Informed on Tax Law Changes

Tax laws are subject to change, and potential legislative actions in the coming years could impact the attractiveness or mechanics of a Roth IRA conversion. It’s crucial to monitor these developments closely.

Subscribing to financial news outlets, consulting with tax professionals, and reviewing IRS publications can help you stay informed. Any changes in federal or state tax rates, or rules regarding retirement accounts, will directly affect your conversion strategy.

Proactive knowledge of these changes allows for timely adjustments to your financial planning, ensuring that your Roth IRA Conversion 2026 remains optimal and beneficial.

| Key Point | Brief Description |

|---|---|

| Tax Implications | Conversion is a taxable event; plan for immediate tax liability. |

| Strategic Timing | Consider lower income years or market downturns for conversion. |

| Future Tax Rates | Roth benefits if you expect higher tax rates in retirement. |

| Professional Advice | Consult a financial advisor for personalized conversion strategies. |

Frequently Asked Questions About Roth IRA Conversions

A Roth IRA conversion involves transferring funds from a traditional, SEP, or SIMPLE IRA into a Roth IRA. This move makes the converted amount subject to income tax in the year of conversion, but future qualified withdrawals and growth become tax-free in retirement, offering significant long-term benefits for retirement savings.

The optimal time for a Roth IRA conversion is generally when you anticipate being in a lower tax bracket than in retirement, or during a market downturn when your IRA’s value is temporarily reduced. This minimizes the immediate tax burden, making your Roth IRA Conversion 2026 more efficient in the long run.

Any pre-tax contributions and earnings converted from a traditional IRA to a Roth IRA are considered taxable income in the year of conversion. This can increase your overall tax liability for that year. It’s crucial to plan for this tax payment from non-retirement funds to maximize your retirement savings.

Yes, a separate five-year rule applies to each Roth IRA conversion. This means that even if your original Roth IRA has been open for more than five years, the converted funds must remain in the Roth IRA for five years before qualified withdrawals of earnings can be made tax-free and penalty-free.

Absolutely. Consulting a qualified financial advisor is highly recommended before undertaking a Roth IRA conversion. They can provide personalized advice based on your unique financial situation, help calculate potential tax liabilities, and ensure the conversion aligns with your overall retirement and estate planning goals for Roth IRA Conversion 2026.

What This Means for Your Retirement Planning

The decision to pursue a Roth IRA Conversion 2026 is a significant one with lasting implications for your retirement savings. It requires careful consideration of your current financial situation, future tax expectations, and overall investment strategy.

As tax laws and economic conditions can shift, staying informed and seeking professional guidance are critical steps. This strategic move can unlock substantial tax-free growth and flexibility in retirement, making it a powerful tool for those who plan meticulously.

Evaluate your options, consult experts, and ensure this decision aligns with your long-term vision for financial security, especially as we approach 2026 and beyond.

Contributions 2026: Limits & Employer Matches")