Decoding Mortgage Rate Trends: 6.8% Average for 2026 Homebuyers

Anúncios

Latest developments on mortgage rate trends 2026, with key facts, verified sources and what readers need to monitor next in Estados Unidos, presented clearly in Inglês (Estados Unidos) (en-US).

Decoding the Latest Mortgage Rate Trends: What a 6.8% Average Means for Homebuyers in 2026 (RECENT UPDATES) is shaping today’s agenda with new details released by officials and industry sources. This update prioritizes what changed, why it matters and what to watch next, in a straightforward news format.

Anúncios

Understanding the 2026 Mortgage Rate Forecast

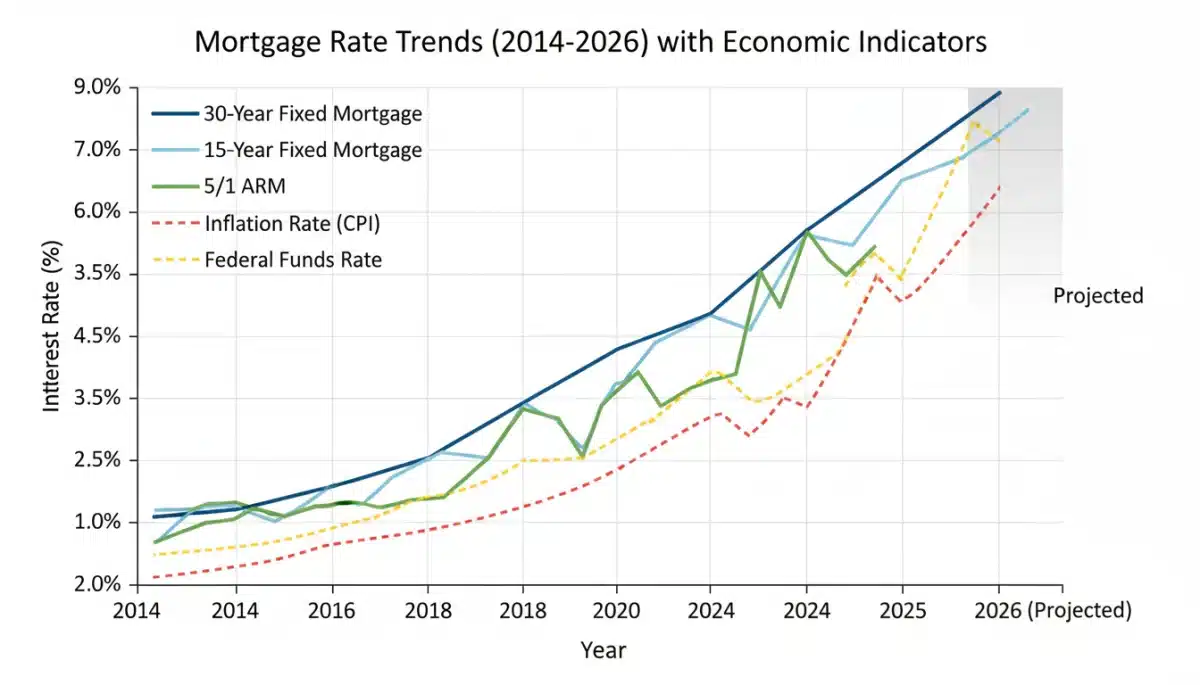

Recent projections indicate that the average 30-year fixed mortgage rate could stabilize around 6.8% by 2026. This forecast, while subject to change, offers a crucial benchmark for individuals planning to enter the housing market.

Economists and financial institutions are closely monitoring various indicators, including inflation, Federal Reserve policies, and global economic stability. These factors collectively influence the trajectory of future mortgage rate trends 2026.

For prospective homebuyers, understanding these underlying dynamics is paramount to making informed decisions. The 6.8% average represents a significant consideration in budgeting and affordability calculations for the coming years.

Anúncios

Key Economic Factors Influencing Rates

Several macroeconomic elements are currently exerting considerable pressure on mortgage rates. Inflationary pressures, though showing signs of moderation, remain a primary concern for central banks, directly impacting lending costs.

The Federal Reserve’s stance on interest rates, particularly the federal funds rate, serves as a foundational element. Any adjustments by the Fed ripple through the financial system, affecting everything from consumer loans to long-term mortgage products.

Additionally, the overall health of the U.S. economy, including employment figures and GDP growth, plays a vital role. A robust economy can sometimes lead to higher rates as demand for capital increases, influencing mortgage rate trends 2026.

Inflation and Central Bank Policies

Inflation continues to be a driving force behind the current interest rate environment. When inflation is high, the Federal Reserve typically raises its benchmark rates to cool down the economy, which in turn pushes mortgage rates upward.

The Fed’s dual mandate of maximum employment and price stability means their decisions are carefully balanced. Future adjustments to monetary policy will be critical in shaping the mortgage rate trends 2026, providing clarity on the path ahead.

Global Economic Landscape and Geopolitical Events

Beyond domestic factors, the global economic landscape and ongoing geopolitical events also contribute to rate volatility. International trade relations, conflicts, and commodity price fluctuations can create uncertainty, prompting investors to seek safer assets, which can influence bond yields and thus mortgage rates.

For instance, disruptions in global supply chains or significant shifts in international financial markets can have a tangible impact on the cost of borrowing for U.S. consumers. These external forces are integral to understanding the broader mortgage rate trends 2026.

Monitoring these global developments is essential for a comprehensive view of where rates might be headed. The interconnectedness of global economies means that events far afield can still have a direct impact on local housing markets and individual financial plans.

Impact on Homebuyers and Affordability

A 6.8% average mortgage rate significantly alters the landscape for potential homebuyers. This rate directly affects monthly payments, influencing how much house individuals can afford and their overall purchasing power.

Higher rates mean that borrowers will pay more in interest over the life of the loan, requiring a larger portion of their income to service the debt. This can lead to adjustments in budget expectations and potentially longer saving periods for down payments.

The affordability challenge is particularly acute for first-time buyers and those in competitive housing markets. Understanding these implications is key to navigating the mortgage rate trends 2026 effectively.

Budgeting for a 6.8% Rate

Homebuyers need to meticulously re-evaluate their budgets in anticipation of a 6.8% average rate. This involves not only calculating the principal and interest but also factoring in property taxes, insurance, and potential private mortgage insurance (PMI).

Financial advisors recommend stress-testing budgets against slightly higher rates to build a buffer. This proactive approach ensures that unexpected fluctuations in mortgage rate trends 2026 do not derail homeownership plans.

Strategies for First-Time Homebuyers

First-time homebuyers face unique hurdles in a higher-rate environment. Strategies such as exploring FHA or VA loans, which often have more lenient qualification requirements, can be beneficial.

Additionally, saving a larger down payment can reduce the loan amount, thereby mitigating the impact of higher interest rates. Understanding available assistance programs is also crucial for navigating the current mortgage rate trends 2026.

Regional Variations in Mortgage Rates and Housing Markets

While a national average of 6.8% provides a general outlook, it is crucial to recognize that mortgage rates and housing market conditions can vary significantly by region. Local economic health, housing supply, and demand dynamics all play a role in these disparities.

Some areas may experience more competitive markets with slightly lower rates due to specific local incentives or a healthier supply of homes. Conversely, rapidly growing or highly desirable regions might see higher property values and potentially tighter lending conditions, influencing the overall mortgage rate trends 2026.

Homebuyers should consult local real estate professionals and lenders to understand the specific nuances of their target market. This localized insight can provide a more accurate picture than national averages alone, helping to tailor financial strategies effectively.

Expert Predictions and Analyst Consensus

Financial experts and housing market analysts generally concur on the trajectory of mortgage rates for 2026, with most predictions hovering around the 6.8% mark. However, there are varying perspectives on the speed and magnitude of any potential shifts in the mortgage rate trends 2026.

Some analysts suggest that if inflation cools more rapidly than expected, there could be room for rates to dip slightly below this average. Others caution that persistent economic resilience or unforeseen global events could push rates higher, maintaining an element of uncertainty.

Consensus reports from major financial institutions like Fannie Mae and the Mortgage Bankers Association provide valuable insights. These reports often highlight the factors they believe will most heavily influence rates, offering a comprehensive view of the expected mortgage rate trends 2026.

Government Policies and Housing Market Support

Government policies at both federal and state levels significantly influence the housing market and mortgage rates. Initiatives aimed at increasing housing supply, such as zoning reform or developer incentives, can indirectly stabilize prices and rates.

Programs designed to assist first-time homebuyers, including down payment assistance or tax credits, also play a vital role in market accessibility. These interventions can help mitigate the impact of rising mortgage rate trends 2026 on affordability.

Regulatory changes impacting lending standards or mortgage insurance requirements can also shape the market. Staying informed about legislative developments is essential for understanding the broader context of housing finance.

Strategies for Navigating Higher Mortgage Rates

With mortgage rate trends 2026 pointing towards a 6.8% average, prospective homebuyers need to adopt strategic approaches to secure favorable financing. One key strategy involves improving credit scores, as a higher score can unlock better loan terms and lower interest rates.

Another effective strategy is to save a larger down payment. A substantial down payment reduces the loan amount, thereby decreasing the total interest paid over time and making monthly payments more manageable, even with higher rates.

Exploring various loan products beyond the traditional 30-year fixed-rate mortgage can also be beneficial. Adjustable-rate mortgages (ARMs) or shorter-term fixed-rate loans might offer lower initial rates, though they come with their own set of risks and considerations for the future mortgage rate trends 2026.

Improving Credit Scores for Better Rates

A strong credit score is a powerful tool in a high-rate environment. Lenders offer the most competitive rates to borrowers with excellent credit histories, reflecting a lower perceived risk. Focusing on paying bills on time, reducing debt, and avoiding new credit inquiries can significantly boost your score.

Regularly reviewing your credit report for errors and disputing any inaccuracies is also crucial. A few points increase in your credit score can translate into substantial savings over the life of a mortgage, directly impacting your experience with mortgage rate trends 2026.

Exploring Different Loan Products

While the 30-year fixed-rate mortgage is popular, other options exist. Adjustable-rate mortgages (ARMs) often start with lower interest rates for an initial period, which can be attractive for those planning to sell or refinance before the adjustment period.

Shorter-term fixed-rate mortgages, such as 15-year loans, typically come with lower interest rates but higher monthly payments. These alternatives can be viable depending on your financial situation and long-term housing goals, especially when considering the projected mortgage rate trends 2026.

The Role of Technology in Mortgage Shopping

Technology is increasingly transforming how homebuyers approach mortgage shopping, especially with dynamic mortgage rate trends 2026. Online mortgage calculators allow individuals to quickly estimate monthly payments, assess affordability, and compare different loan scenarios without extensive manual calculations.

AI-powered platforms and aggregators provide personalized rate comparisons from multiple lenders, streamlining the process of finding the best deal. These tools can analyze a borrower’s financial profile and instantly match them with suitable loan products, saving time and effort.

Virtual consultations with mortgage advisors and online application portals also enhance convenience and accessibility. Leveraging these technological advancements can empower homebuyers to make more informed and efficient decisions in a fluctuating rate environment.

| Key Point | Brief Description |

|---|---|

| 2026 Rate Forecast | Average 30-year fixed mortgage rates projected at 6.8%. |

| Economic Influences | Inflation, Fed policy, and economic growth drive rate changes. |

| Homebuyer Impact | Higher rates affect affordability and monthly payment calculations. |

| Strategic Planning | Improve credit, save larger down payments, explore loan options. |

Frequently Asked Questions About 2026 Mortgage Rates

Current expert consensus suggests the average 30-year fixed mortgage rate could be around 6.8% by 2026. This forecast is based on various economic indicators, but it remains subject to potential shifts in market conditions and Federal Reserve policies.

A 6.8% rate will result in higher monthly payments compared to lower rates. For example, on a $300,000 loan, a 6.8% rate means significantly more interest paid over the loan’s life, impacting overall affordability and increasing your debt service burden.

Key drivers include inflation, the Federal Reserve’s monetary policy decisions, and the overall strength of the U.S. economy. Geopolitical events and global market stability also play a role in shaping the direction of these mortgage rate trends 2026.

Homebuyers should focus on improving their credit scores, saving for a larger down payment, and exploring different loan products. Consulting with a financial advisor to personalize strategies for navigating the mortgage rate trends 2026 is also highly recommended.

Yes, while national averages provide a benchmark, local housing market conditions, supply-demand dynamics, and economic health can lead to regional variations. It’s important to research specific local market conditions when considering the broader mortgage rate trends 2026.

Looking Ahead: Implications for the Housing Market

The projected mortgage rate trends 2026, particularly the 6.8% average, will continue to shape the housing market significantly. Homebuyers will need to remain agile and well-informed, adapting their strategies to prevailing economic conditions. Monitoring Federal Reserve announcements, inflation data, and global economic shifts will be paramount for anyone considering a home purchase in the coming years. This environment underscores the importance of robust financial planning and seeking expert advice to navigate the evolving landscape effectively.